Can You Retire at 55? Early Retirement Math Tips

April 17, 2026

Can You Retire at 55? A Realistic Look at the Math

We’ve all had that Tuesday morning where we stared at the alarm clock and wondered, “What if I just didn’t go in?” Leaving the workforce at 55 sounds like the ultimate cure for career burnout and a step toward financial independence, but shifting that timeline forward by a decade changes the financial rules entirely. While the dream of early freedom and early retirement is common, making the numbers work requires a very different strategy than the standard retirement plan most of us grew up hearing about.

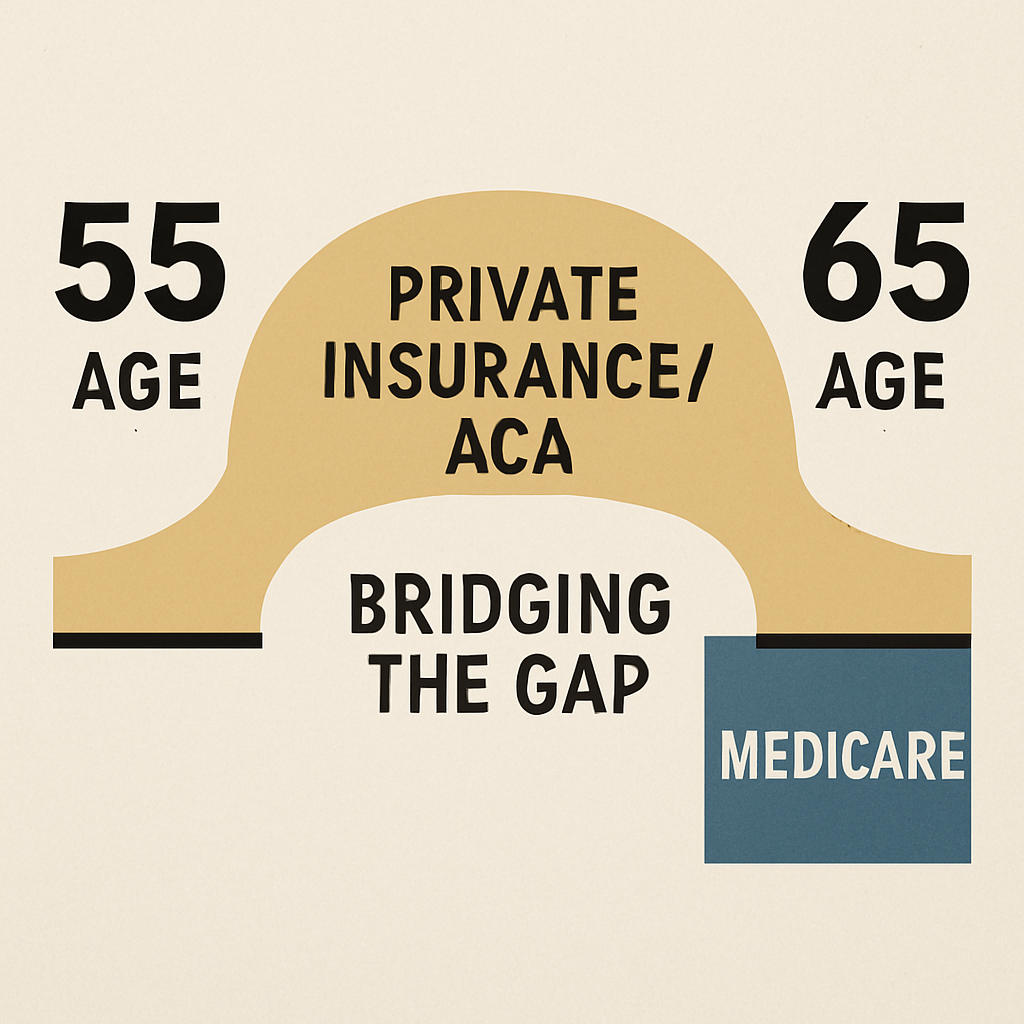

The biggest hurdle isn’t necessarily saving enough money for your eighties; it is surviving the “10-Year Gap.” Since you generally cannot access Medicare until 65 or full Social Security benefits until later, retiring at 55 means you are essentially self-funding a full decade of life. You need to cover every grocery bill, property tax, and health insurance premium out of pocket before the traditional safety nets finally kick in to help support you.

Determining feasibility requires thinking of your retirement fund not as a complex investment portfolio, but simply as a household water tank. You need to know exactly how much water is currently in the tank, how much is leaking out every month through spending, and whether the reserve is big enough to last the night without rain. If the leaks are too big or the tank is too small, the supply runs dry long before morning comes.

You don’t need a finance degree to solve this equation. Figuring out if you can retire at 55 comes down to solving for just three specific numbers unique to your life. The math reveals whether an early exit is a realistic milestone or just a pleasant daydream.

The Multiplier Method: How to Calculate Your Target Nest Egg

You might have a vague goal to “save as much as possible,” but that strategy is like driving cross-country without a map. To know if you can clock out for good at 55, you need a specific finish line. While financial planners often use complex simulations to answer “how much do I need to retire at 55,” you can determine your own target with a straightforward calculation that requires nothing more than fourth-grade math.

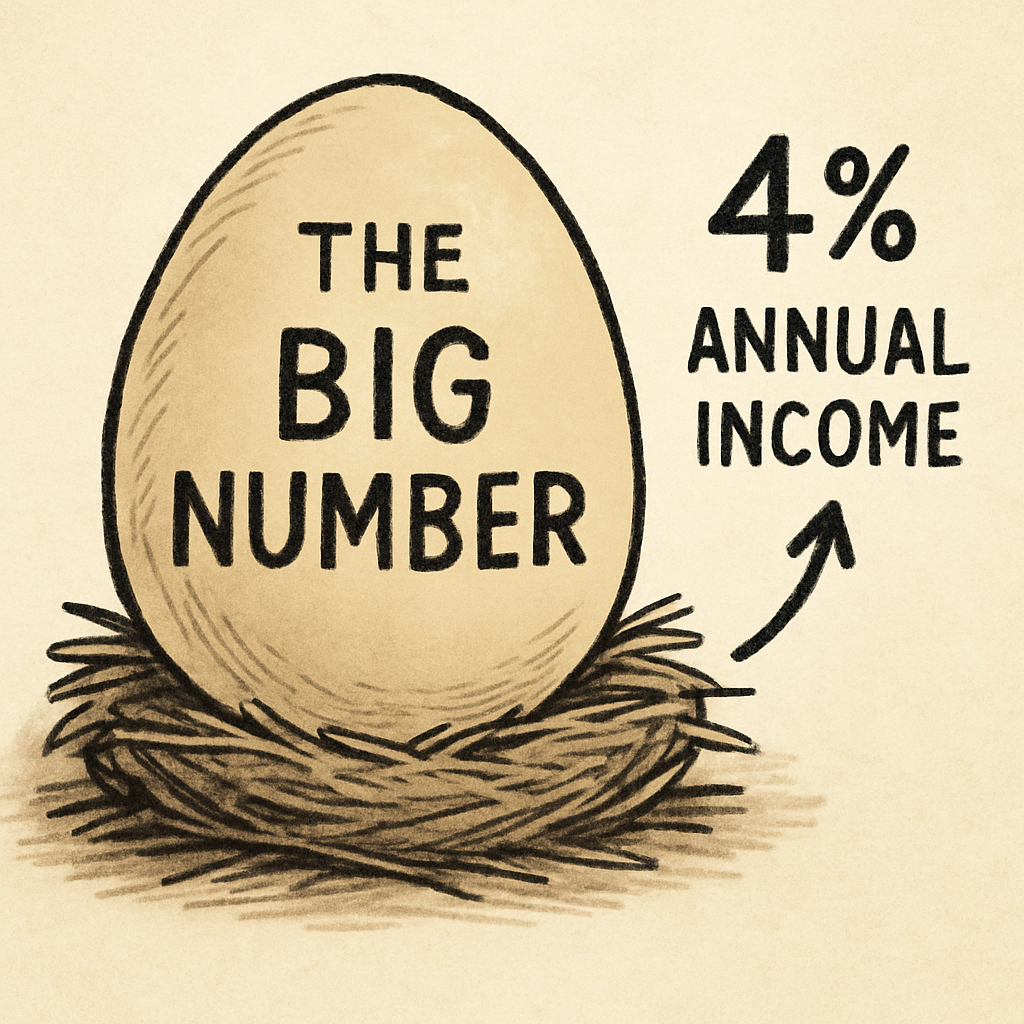

This shortcut is known as the Rule of 25. It suggests that you need to accumulate 25 times your annual expenses to retire safely. If you have already tracked your yearly spending, finding your “Big Number” takes less than a minute:

- Determine your annual spend (e.g., $50,000).

- Multiply that number by 25.

- The result ($1.25 million) is your target Nest Egg.

Why does this specific multiplier work? The Rule of 25 is the inverse of the “4% Rule,” a standard benchmark for a safe withdrawal rate for early retirement. Think of this as an “Interest-Only Strategy”: if you withdraw 4% of your portfolio to live on, and your investments grow by an average of 7% over time, your principal balance should remain stable or even grow. This basic framework is the most reliable method for calculating retirement nest egg longevity without running out of money in your 80s.

However, having $1.25 million in a 401k doesn’t automatically mean you can retire at 55. Standard retirement accounts usually charge a steep 10% penalty if you access the funds before age 59½. Since you plan to leave the workforce four years early, you need a specific legal strategy to bridge that gap without handing a chunk of your hard-earned savings over to the IRS.

How to Tap Your 401k at 55 Without Paying IRS Penalties

The biggest logistical headache for the 55-year-old retiree isn’t usually saving the money, but accessing it. Most retirement accounts are designed to stay locked until age 59½, and crossing that line early typically triggers a painful 10% penalty on top of regular income taxes. Losing $5,000 of every $50,000 withdrawal to an easily avoidable fee can devastate your safe withdrawal rate, but the IRS offers three specific exceptions designed for early departures.

For those leaving their jobs in the calendar year they turn 55 or older, the most direct path is the “separation from service” exception. Often called the Rule of 55, this provision allows you to withdraw funds from your current employer’s 401 (k) without penalty immediately after quitting. Crucially, the IRS Rule 55 guidelines apply only to the 401 (k) at the job you just left, not to old accounts from previous employers or personal IRAs.

If your savings are already sitting in an IRA, you need a different key to unlock the door. You can utilize Rule 72(t) substantially equal periodic payments (SEPP), which allows penalty-free access to IRAs at any age, provided you commit to a rigid withdrawal schedule. This method is essentially a contract with the IRS: you agree to take out a calculated amount every single year for at least five years or until you turn 59½, whichever is longer.

Choosing between these options depends largely on where your money is currently parked:

- Flexibility: Rule 55 allows you to take out whatever you need whenever you need it; Rule 72(t) locks you into a strict annual amount that cannot be changed without retroactive penalties.

- Account Type: Rule 55 works exclusively with your most recent employer’s 401k; Rule 72(t) is generally best suited for IRAs.

- Timing: Rule 55 requires leaving your job at age 55+; Rule 72(t) can be started earlier.

A final, less common tactic applies if your company matched your contributions with company stock rather than cash. The net unrealized appreciation strategy (NUA) allows you to pay lower capital gains tax rates on the growth of that stock rather than higher income tax rates. Understanding these mechanisms ensures you avoid tax penalties on early 401 (k) withdrawals, keeping your money in your pocket where it belongs. Once you have secured your cash flow, your next challenge is protecting that income from the skyrocketing costs of private insurance.

Solving the $20,000 Healthcare Problem Before Medicare

Leaving the workforce at 55 means walking away from employer-subsidized health insurance a full decade before Medicare eligibility begins. While the law allows you to keep your current plan through COBRA for up to 18 months, you will likely face sticker shock when you see the full premium price without your boss chipping in. For a typical couple, this expense can easily exceed $20,000 a year, rapidly draining the savings you worked so hard to unlock.

The Affordable Care Act (ACA) marketplace usually offers a more sustainable long-term solution, especially if you can manage your reported income. Because early retirees often live off savings that have already been taxed or generate lower taxable income, they frequently qualify for significant subsidies that reduce monthly premiums. By carefully controlling how much you withdraw from taxable accounts versus tax-free sources, you can effectively lower your insurance bill to match a much smaller budget.

Ideally, you have been funding a Health Savings Account (HSA) during your working years, which serves as the ultimate bridge for these medical expenses. Financial planners often call the HSA “triple-tax advantaged” because the money goes in tax-free, grows tax-free, and comes out tax-free if used for qualified medical costs. Using this dedicated bucket for premiums and doctor visits preserves your main retirement fund for housing and food, acting as a specialized shield against rising healthcare costs.

Securing affordable healthcare is only half the battle; the other half is ensuring your main nest egg doesn’t shrink too fast. Even with insurance costs under control, a sudden economic downturn right after you quit can force you to sell investments at a loss, permanently damaging your portfolio’s ability to recover.

Why a Market Crash in Year One Can Break Your Math

Imagine retiring on a Friday, and the stock market crashes on Monday. If you were still working, you would simply wait for your 401 (k) to bounce back, but once you rely on that money for groceries, you lose the luxury of patience. Selling investments when their value is down is dangerous because you have to sell more shares just to generate the same amount of cash to pay your mortgage and bills.

Financial planners call this danger “Sequence of Returns Risk,” but think of it as the specific hazard of a bad start. If your $1,000,000 nest egg drops to $800,000 in year one, and you withdraw your standard $40,000 for annual spending, you are digging a hole that is mathematically difficult to escape. The remaining investments must achieve extraordinary growth just to get you back to where you started, significantly increasing the odds that you will run out of money later in life.

To sleep better at night, many early retirees build a defensive “Cash Bucket” before handing in their resignation notice. This strategy involves keeping one to three years of living expenses in a stable, high-yield savings account rather than the stock market. When stocks are performing well, you sell shares to pay for your life; when the market dives, you stop selling shares completely and spend from your cash reserves until prices recover.

Surviving these critical first few years without selling at a loss sets the trajectory for the rest of your freedom, effectively buying your portfolio time to heal. Once you have navigated the immediate risks of market volatility, you must turn your attention to the slow, invisible erosion of your purchasing power caused by decades of rising prices.

The Shrinking Dollar: Adjusting Your Plan for 30+ Years of Inflation

While a stock market crash feels like a sudden storm, inflation acts more like termites in your foundation. It eats away at your “purchasing power”—the amount of goods you can buy with a specific amount of money—so slowly that you might not notice until the damage is severe. If you retire at 55 with a fixed income that covers your bills comfortably today, that same dollar amount will likely leave you struggling to pay for basics by the time you reach your late 70s.

Estimate how quickly your expenses will double using a handy mental shortcut called the “Rule of 72.” Simply divide 72 by the expected inflation rate to see how many years it takes for your money to lose half its value. At a historical average of 3% inflation, the cost of living doubles every 24 years, meaning your nest egg must remain invested in assets that grow aggressively enough to give you a “raise” every single year.

To visualize this impact on your inflation-adjusted retirement income planning, consider how everyday prices might look just two decades into your retirement compared to now:

- Loaf of Bread: $3.00 today → $5.42 in 20 years

- Gallon of Gas: $3.50 today → $6.32 in 20 years

- Basic Sedan: $25,000 today → $45,150 in 20 years

Since your personal savings must constantly battle this erosion, it becomes critical to maximize the one income source that automatically adjusts for inflation for the rest of your life.

Social Security: The Permanent Cost of Claiming at 62 vs. 67

Many early retirees plan to file for benefits at 62 to ease cash flow, but this decision comes with a permanent price tag. The government designates a specific “Full Retirement Age” (FRA), typically 67 for those born in 1960 or later, which is when you earn 100% of your promised payout. Claiming five years early results in a benefit reduction of roughly 30%, locking in a significantly smaller income stream for the rest of your life.

Think of delaying your claim as buying insurance against outliving your money. A standard $2,000 monthly benefit at age 67 shrinks to just $1,400 if you start at 62, costing you tens of thousands of dollars over a long retirement. While taking money early relieves pressure on your personal savings initially, waiting ensures a larger, inflation-proof safety net when you are older and potentially facing expensive health challenges.

Your ability to wait hinges on the strength of your “bridge fund,” the personal savings designated to cover bills before government benefits kick in. If your nest egg can support your household until age 67, delaying Social Security acts as a powerful strategy to maximize your guaranteed income. With the variables of inflation and benefits now clear, you are ready to build a concrete timeline.

Your 30-Day Early Retirement Action Plan

Retiring early isn’t about luck; it is a calculation of life years purchased. For many, it’s also a deliberate path to financial independence. You no longer need to guess if Can You Retire at 55. A Realistic Look at the Math applies to you- you now possess the framework to verify it. By understanding the “Gap Years” between 55 and Social Security, and knowing that your nest egg must replace your paycheck entirely during that decade, the vague dream of freedom transforms into a specific financial target.

Moving from theory to action requires committing to this 30-day “Reality Audit” with a few practical financial planning tips to see exactly where you stand:

- Track Every Penny: Log all household spending for one month to find your true annual burn rate.

- Price the Gap: Research the current cost of a private Bronze or Silver health insurance plan for a 56-year-old in your zip code to estimate future healthcare costs.

- Check the Rules: Review your current 401(k) summary description to confirm it allows for “Rule of 55” penalty-free withdrawals.

- Calculate Your Number: Multiply your annual spending by 25 to see the total nest egg required for long-term safety.

Early retirement is strictly a function of the gap between what you spend and what you have saved. If the numbers look daunting today, remember that clarity is the only way to close that gap. Start simple. Before you worry about investment returns or tax strategies, focus entirely on that first checkbox. Open your banking app and start tracking your spending today—because you cannot escape the rat race until you know exactly how much it costs to buy your way out on the path to financial independence.

Want to know if retiring at 55 is realistic for you?

Schedule a free, no-obligation consultation, and we’ll help you run the numbers—income needs, healthcare gap, withdrawal rate, and timeline, so you can see what’s possible and what needs to change.