Tax-Efficient Retirement Strategy: Maximize Savings

April 20, 2026

Tax-Efficient Retirement Strategy: Keep More of Your Savings

Imagine spending decades building a nest egg, only to realize a silent partner owns a significant percentage of it. This partner waits patiently while your money grows, retaining the legal right to decide their cut when you finally start withdrawing funds. For millions of savers, this partner is the IRS. This Tax-Efficient Retirement Strategy: How to Keep More of What You Saved guide outlines practical retirement income strategies rooted in tax-efficient investing to support smarter retirement planning.

While your 401k statement might display a milestone balance of $1 million, that number represents gross savings rather than spendable income. Financial professionals often remind clients that if your future tax bracket is 25%, your actual purchasing power is really only $750,000.

Traditional retirement planning usually relies on “tax-deferred” growth, which functions essentially as a postponement rather than a savings. You receive a tax break today, but the bill effectively accrues interest alongside your investments, waiting for you to retire.

A tax-efficient retirement strategy allows you to buy out this silent partner on your own terms. By understanding the balance between tax-deferred and tax-exempt retirement accounts, you can structure your withdrawals to keep more of what you earned. These ideas fit within broader retirement income strategies designed to control how and when you recognize income.

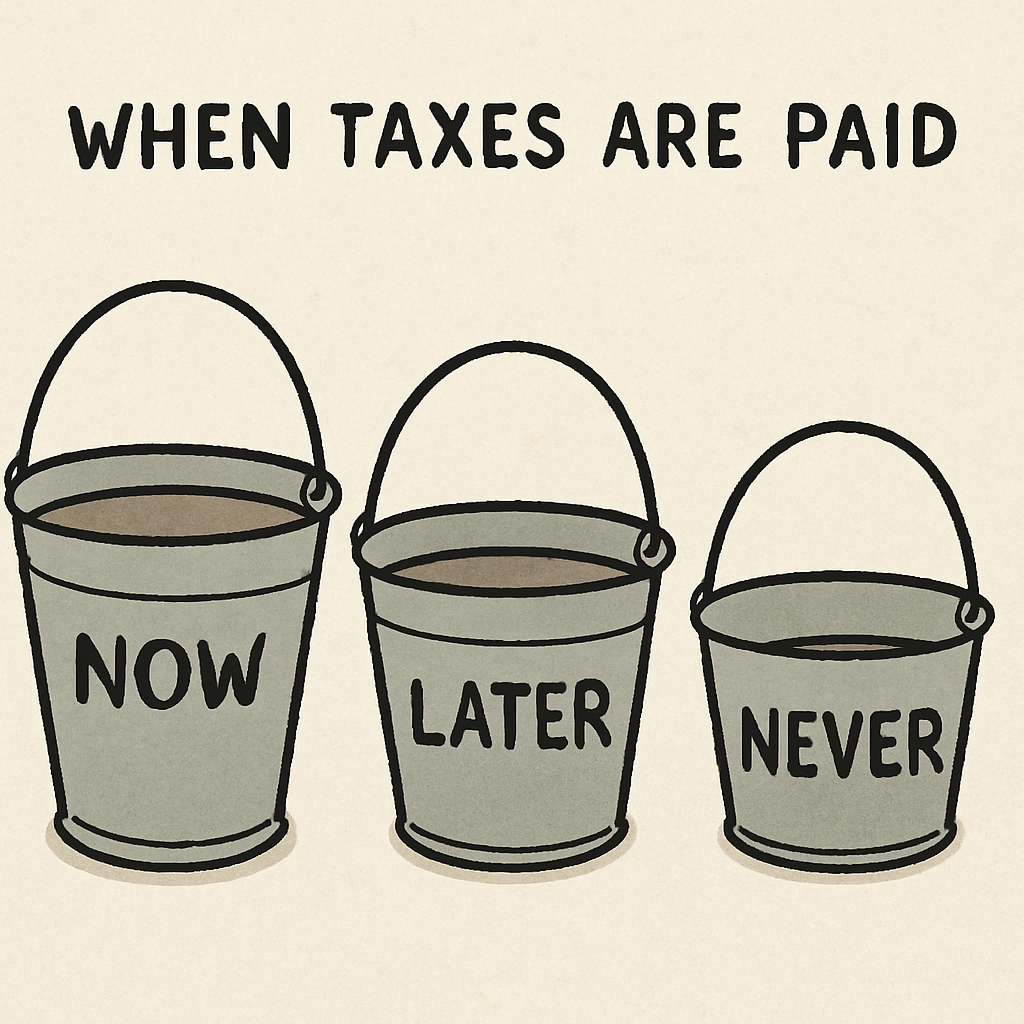

The Three-Bucket Strategy: Building a Shield Against Future Tax Hikes

Relying entirely on a traditional 401k creates a rigid path for your future income. While watching that balance grow is satisfying, it often leads to a “tax trap” where every single withdrawal is taxed as ordinary income. If tax rates rise by the time you retire, your purchasing power drops immediately because you lack alternative funding sources to pay for your lifestyle.

Breaking out of this trap requires a concept called asset location for tax efficiency, a core tenet of tax-efficient investing. Instead of viewing your savings as one large pile of money, visualize your portfolio as three distinct buckets characterized by when the IRS collects its share.

- Taxable (The “Now” Bucket): Standard brokerage and bank accounts. You pay taxes on interest and dividends annually, but the money is accessible without penalty.

- Tax-Deferred (The “Later” Bucket): Traditional 401 (k) s and IRAs. You get a tax deduction today, but the government takes its cut when you withdraw funds in retirement.

- Tax-Free (The “Never” Bucket): Roth IRAs and HSAs. You pay taxes on the income before contributing, allowing the money to grow and withdraw without triggering a new tax bill.

By maintaining balance across these categories, you gain control over how much income you report to the IRS in any given year. You might withdraw from tax-deferred accounts just enough to fill a low tax bracket, then fund the rest of your spending with tax-free cash. This flexibility is the cornerstone of a highly effective strategy.

Deciding which bucket to prioritize depends on a calculation regarding your current versus future tax rates. It ultimately comes down to a fundamental question about growth potential: is it better to pay the tax on the seed or the harvest?

The Seed vs. The Harvest: Should You Pay Taxes Now or Later?

Farming wisdom offers the clearest answer to this dilemma. When you choose a Roth account, you volunteer to pay taxes on your “seed”—the initial contribution—while it is still a small, known amount. Since you have already settled your debt with the IRS, every dollar of growth over the next twenty years belongs entirely to you. This approach effectively locks in today’s tax rates, shielding your portfolio from legislative changes that might increase costs by the time you are ready to retire.

Conversely, selecting a traditional 401k focuses on tax postponement, providing an immediate break on your current annual bill. While this deduction boosts your take-home pay today, it means the government retains a claim on your entire future harvest, including decades of compound interest. If you expect your income to drop significantly in your golden years, this trade-off works in your favor; however, if general tax rates rise, you are simply deferring your liability into a much more expensive environment.

Determining the winner between a Roth and a traditional 401k ultimately relies on comparing your marginal tax rate today against your projection for tomorrow. If you are currently in a lower earning phase, paying the tax now usually yields better long-term results than gambling on uncertain future rates. Success requires managing tax brackets carefully, and once you have accumulated these savings, the specific order in which you spend them becomes the next critical factor in preserving your wealth.

The Smart Withdrawal Sequence: Why Spending Your Cash First Could Save You $50,000

Most people assume that a dollar is worth the same amount regardless of which account it sits in, but withdrawing funds from the wrong bucket at the wrong time can trigger unnecessary bills that shorten your money’s lifespan. Just as you carefully planned how to save, you must now prioritize the order in which you spend down your assets. A strategic approach prevents you from pushing yourself into a higher tax bracket and preserves your capital for future growth.

By leaving your tax-sheltered accounts alone for as long as possible, you allow them to continue compounding without immediate IRS interference. This strategy relies on a standard tax-efficient withdrawal sequence, designed to keep your adjusted gross income low in the early years of retirement while your most powerful assets grow in the background. As part of thoughtful retirement income strategies, this approach can improve after-tax outcomes without increasing investment risk.

Financial planners generally recommend, as part of retirement income strategies, tapping into your three distinct buckets in this specific order to maximize efficiency:

- Taxable Accounts: Sell investments in standard brokerage accounts first, as capital gains taxes are typically lower than income tax rates.

- Tax-Deferred Accounts: Withdraw from Traditional IRAs and 401(k)s next, but only enough to fill up lower tax brackets.

- Tax-Free Accounts: Save Roth IRAs for last, allowing them the longest possible runway for tax-free growth.

Adhering to this hierarchy is essential for minimizing taxes on retirement income and can extend the life of your portfolio by several years. However, simply following this list isn’t enough if you ignore how these withdrawals interact with government benefits; failing to watch your income thresholds can trigger the infamous “Tax Torpedo” that eats away at your Social Security checks.

How to Defuse the ‘Retirement Tax Torpedo’ and Keep Your Social Security Check Whole

Many retirees are shocked to discover that withdrawing just $1 too much from a 401(k) can suddenly make up to 85% of their Social Security check taxable. This phenomenon, often called the “Tax Torpedo,” occurs because the IRS looks at your combined revenue streams to determine your tax bill. Avoiding the retirement tax torpedo requires understanding that your benefits are not taxed in a vacuum; they are taxed based on how much other money you generate in a single year.

To figure out if you are in the danger zone, you must calculate your “Provisional Income”—a specific IRS formula that combines your Adjusted Gross Income, tax-exempt interest, and half of your Social Security benefit. Understanding how social security benefits are taxed at these specific levels allows you to keep your income in the “sweet spot.” Here are the current thresholds where taxation kicks in:

- Single Filers: Benefits are generally tax-free if provisional income is under $25,000.

- Married Filing Jointly: Benefits are generally tax-free if provisional income is under $32,000.

Because withdrawals from traditional IRAs count toward these limits, taking out extra cash for a renovation could inadvertently spike your tax rate significantly. Optimization often means pulling from tax-free sources like a Roth IRA when you are near these thresholds to prevent triggering the torpedo. However, you can only control these withdrawals until age 73, at which point the government mandates you take money out, potentially forcing you into a tax trap you can’t escape.

Mastering Roth Conversions to Avoid the ‘Government-Forced’ Tax Spike at Age 73

Most retirees enjoy full control over their funds until age 73, when the government steps in to demand its share of their deferred savings. These Required Minimum Distributions (RMDs) force you to withdraw a specific percentage of your pre-tax accounts annually, regardless of whether you actually need the cash for expenses. If you have been a diligent saver, these mandatory withdrawals can artificially inflate your income, inadvertently pushing you into a higher bracket and triggering the very tax torpedo you tried to avoid.

To prevent this forced income spike, savvy investors utilize the “Tax Valley”—the strategic window between retirement and age 73 when your taxable income is naturally lower. During these low-income years, you can execute a Roth conversion, which involves moving funds from a traditional IRA to a Roth IRA and paying income tax on the transfer immediately. While voluntarily paying taxes sounds counterintuitive, managing your tax brackets this way allows you to pay a known low rate on the “seed” today rather than a higher, forced rate on the “harvest” later.

Systematically converting these funds reduces the size of your pre-tax nest egg, which directly lowers the mandatory distributions you must take in your 70s. When weighing the pros and cons of Roth conversions, the primary benefit is mathematical certainty: you eliminate the risk of rising future tax rates while avoiding RMD tax penalties on your excess savings. Once you have maximized these conversion opportunities, you can look toward specialized assets like Health Savings Accounts and municipal bonds to further diversify your tax-free income streams.

Hidden Gems: Using HSAs and Municipal Bonds for 100% Tax-Free Income

While Roth IRAs often steal the spotlight, the Health Savings Account (HSA) is arguably the most powerful tool in a tax-efficient retirement strategy. Most savers treat these as short-term spending accounts, but if you pay current medical bills out-of-pocket, the HSA becomes a “Super-Roth,” offering a unique triple threat:

- Contributions are tax-deductible immediately.

- You enjoy tax-free growth over the long term.

- Withdrawals for qualified medical expenses are completely tax-free.

For income needs outside of healthcare, municipal bonds serve as another critical shield. Unlike corporate bonds or savings accounts, where interest is taxed as ordinary income, “munis” generally pay interest that is free from federal taxes. This allows you to generate spendable cash flow without inflating the income metrics that determine your tax bracket or Medicare costs.

Integrating these tax-free revenue streams ensures that your lifestyle is funded by your wealth rather than eroded by the IRS. As you secure your own financial future, the final piece of the puzzle is ensuring those assets transfer efficiently to your heirs without triggering unnecessary surcharges.

Protecting Your Legacy: The Step-Up in Basis and Avoiding Medicare Premium Surcharges

Success in retirement comes with a hidden penalty if your yearly income climbs too high. The government uses your tax return from two years before to set your healthcare costs, and crossing specific thresholds triggers Medicare Part B IRMAA surcharges, which function simply as extra monthly premiums for the same coverage. This cliff effect means withdrawing just one extra dollar from a standard IRA could accidentally push you into a bracket that costs you thousands in added fees, making precise income monitoring essential.

Strategic planning also ensures your generosity doesn’t burden your loved ones with a surprise bill. If you sell highly appreciated stock today, you owe capital gains taxes on the profit, but holding those same assets until death triggers a “reset” on their value for your beneficiaries. This step-up in basis for inherited assets allows heirs to sell the stock immediately tax-free, erasing decades of potential tax liability in a single moment.

For retirees facing forced withdrawals they don’t need for living expenses, philanthropy offers a powerful escape valve. You can send funds directly to a non-profit via Qualified Charitable Distributions from IRA accounts, which satisfies the government’s mandatory distribution requirement without ever adding a cent to your taxable income. With these protective measures understood, you are ready to build your personal roadmap.

Your 4-Step Action Plan to Plug the Tax Leaks in Your Retirement Bucket

You now see your savings not just as a pile of money, but as distinct buckets with specific rules. Building a tax-efficient retirement strategy isn’t about earning higher returns; it is about plugging the holes where your wealth leaks out. You finally have the knowledge to stop treating the IRS as a silent partner who decides its own share.

Turn this insight into action with this retirement planning checklist:

- Audit Your Buckets: Check if you are over-exposed to fully taxable accounts.

- Forecast Your Valley: Identify low-income years for potential Roth conversions.

- Check Torpedo Risk: Calculate if withdrawals will trigger taxes on Social Security.

- Maximize HSAs: Automate contributions for triple-tax advantages.

Minimizing taxes on retirement income is ultimately about control. Pull out your latest tax return alongside your account balances this weekend. By adjusting where your savings go today, you ensure you keep more of the harvest you worked a lifetime to grow.

Want to keep more of what you’ve saved, without guessing on taxes?

Schedule a free, no-obligation consultation, and we’ll help you review tax risks, identify smarter withdrawal sequencing, and outline practical steps to improve long-term efficiency.