Life Insurance & Annuities: Protect Your Family, Secure Your Retirement

April 13, 2026

Life Insurance and Annuities: What Each One Is Designed to Do

Most financial plans hinge on two opposing questions: What happens to my family if I’m gone tomorrow? And conversely, what happens if I live to be 100? This guide, Life Insurance and Annuities: What Each One Is Designed to Do, keeps the comparison straightforward and practical. While they are often sold by the same companies, an annuity and life insurance are mirror images of one another (often discussed as annuity and life insurance). One addresses the specific fear of dying too soon, while the other tackles the increasingly common risk of outliving your savings.

Life insurance acts as an umbrella, providing immediate cash to pay off a mortgage or replace a salary if the unthinkable happens. An annuity, however, operates like a personal pension or a steady stream, designed to turn a pile of savings into a guaranteed paycheck that lasts for life. With modern medicine extending our timelines, managing retirement longevity risk requires understanding that one tool protects your legacy, while the other preserves your lifestyle.

Protecting Your Family’s Tomorrow: Why Life Insurance is Your Financial Umbrella

If you are the primary earner, your paycheck is the engine keeping the household running. When that engine stops, protecting heirs with life insurance becomes the only way to generate an immediate financial replacement. This coverage creates an “instant estate,” a significant pool of money that didn’t exist yesterday but is available today to support the people you love. This safety net ensures that your family’s financial timeline remains intact even if yours is cut short.

The process relies on specific beneficiary designation rules to ensure the money creates stability rather than conflict. You simply designate a recipient, the person or trust you choose to receive the funds, and the insurance company delivers a lump sum known as the death benefit. Unlike many other financial transfers, this payout generally arrives income-tax-free, allowing your loved ones to use the full amount for immediate expenses without the IRS taking a share.

Among common life insurance types, term coverage focuses on pure protection at typically lower premiums, while permanent policies can build cash value over time and provide added flexibility.

Guessing a coverage amount, such as an arbitrary one million dollars, often leaves gaps in your protection. Financial professionals often recommend the “DIME” method to capture the full picture:

- Debt: Total up credit cards, car loans, and private student loans.

- Income: Multiply your annual salary by the number of years your family needs support.

- Mortgage: Include the entire remaining payoff balance on your home.

- Education: Estimate future tuition and board costs for your children.

With those calculations set, you have effectively solved the problem of leaving your family too soon. The opposite financial risk challenges us next: the struggle of living longer than your savings account.

Securing Your Own Paycheck: How Annuities Build a Bridge to a Worry-Free Retirement

While life insurance protects your loved ones if you leave early, annuities protect you if you stick around for a long time. In brief, annuities explained that an annuity functions as a “do-it-yourself pension.” You provide a lump sum of savings to an insurance company, and in return, they contractually agree to send you a steady paycheck. This arrangement specifically targets the modern retiree’s biggest fear: outliving retirement savings.

Social Security usually covers the basics, but it rarely covers the full cost of a comfortable lifestyle. By establishing guaranteed lifetime income streams through an annuity, you effectively purchase “longevity insurance.” Whether you live to 85 or 105, the checks continue to arrive, acting as a reliable supplement to your 401(k) or IRA. This creates a financial floor that market crashes or economic downturns cannot remove, ensuring you can pay the bills regardless of stock market performance.

Choosing the right vehicle depends on your appetite for risk versus your need for certainty. Most contracts fall into two primary categories to match these preferences:

- Fixed Annuities: Offer a specific, guaranteed interest rate, prioritizing safety and predictability over aggressive growth.

- Variable Annuities: Invest your premiums in the market (similar to mutual funds), offering higher growth potential but coming with the risk of fluctuating value.

Timing also plays a crucial role. You can select immediate vs deferred payout options depending on whether you need income starting next month or want the account to grow tax-deferred for another decade. Life insurance creates cash when you die, while annuities distribute cash while you live; distinct roles for distinct phases of life.

Direction Matters: Comparing the Flow of Money in Insurance vs. Annuities

When comparing life insurance and annuities, the fundamental difference between these two financial tools lies in who actually receives the check. Life insurance is designed as a “death benefit,” acting as an immediate financial safety net for your heirs when you are no longer around to provide for them. Conversely, annuities function as a “living benefit” primarily designed for you. While insurance creates a pool of money to replace your lost wages, an annuity distributes a pool of money to ensure you do not outlive your savings.

How these funds are delivered also changes based on the vehicle you choose. Most life insurance policies pay out a tax-free lump sum, giving your family the immediate flexibility to pay off a mortgage or fund college tuition in a single transaction. Annuities typically reverse this flow by converting your accumulated savings into a steady stream of periodic payments, monthly or quarterly income that mimics the reliability of a salary during your retirement years.

The following breakdown clarifies their primary roles:

| Feature | Life Insurance | Annuities |

| Primary Goal | Protection for your family through a death benefit | Income for you through a living benefit |

| Risk Managed | Dying too soon | Living too long |

| Typical Payout | One-time lump sum | Monthly income stream |

After determining the direction your money needs to flow, maximizing how much you keep requires understanding the specific tax advantages of each “bucket.”

The ‘Bucket’ Strategy: Understanding Tax Benefits and Cash Value Accumulation

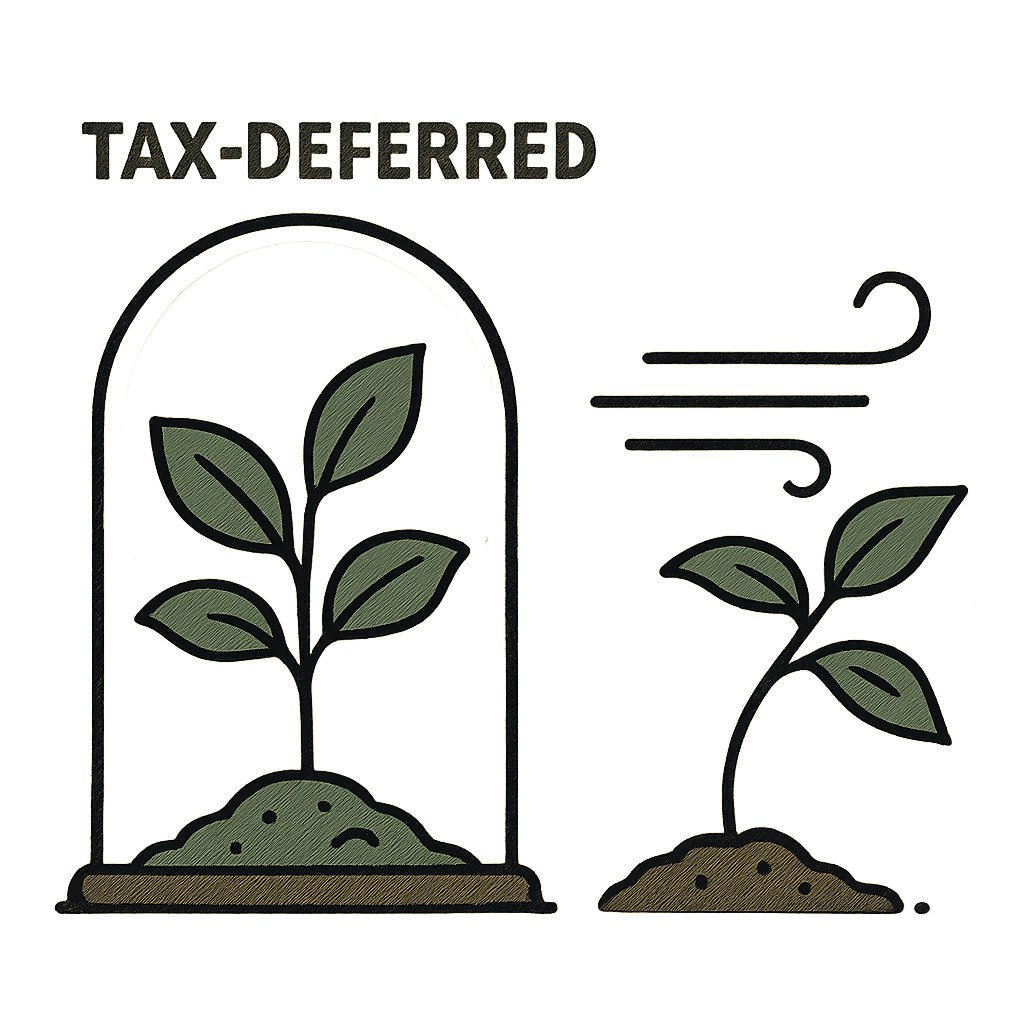

Putting money aside for the future is hard enough without the IRS tapping the brakes on your progress every April. In a standard savings or investment account, you are typically required to pay taxes on any interest or dividends you earn that year, even if you reinvest them. This annual friction reduces the total balance available to generate returns for the following year, slowing down the compounding process significantly.

Annuities and permanent life insurance policies offer shelter from this yearly tax bill through tax deferral. Much like growing a garden inside a protective glass dome, the harsh “weather” of annual taxation cannot get in, leaving your money free to grow uninterrupted. You generally only pay taxes on the gains when you finally withdraw the funds, allowing your interest to earn interest on the full principal amount for years or even decades.

Permanent life insurance policies add another layer of utility by building “cash value,” which functions like a savings account embedded within your coverage. A portion of every premium payment is directed into this bucket, where it accumulates over time. Unlike the death benefit, which is reserved for your heirs, this cash value is a living benefit accessible to you, providing a reservoir of funds you can borrow against for emergencies or retirement supplements.

While the ability to compound growth without immediate tax drag is a significant advantage, these “buckets” are not as liquid as a standard checking account. Insurance companies design these products for long-term stability, meaning early access to your money often comes with strict limitations.

Navigating the Fine Print: Surrender Charges, Penalties, and Beneficiary Rules

Because insurance companies invest your money for the long haul to support those guaranteed future payouts, they require a firm commitment in return. If you decide to withdraw your funds or cancel the contract during the early years, typically the first 5 to 10 years, you will face a “surrender charge.” This acts as a breakage fee for ending a lease early, allowing the insurer to recoup its setup costs. Furthermore, the IRS enforces its own discipline on these tax-deferred vehicles: withdrawing earnings from an annuity before age 59 usually triggers a 10% federal tax penalty on top of standard income taxes, making these tools strictly for long-term planning.

Beyond the financial mechanics, the most critical administrative step is clearly defining who inherits the account. While most people remember to name a “primary beneficiary,” such as a spouse, life can be unpredictable. You must also designate a “contingent beneficiary,” a backup, such as a child or a trust, that receives the funds if the primary beneficiary passes away before you do. Neglecting this step or failing to update names after major life events like a divorce can send your money into a lengthy legal process called probate, delaying support for your family when they need it most.

Before finalizing any policy, perform this quick protection audit:

- Check the Timeline: How many years does the surrender charge period last?

- Know the Cost: What is the penalty percentage if you need to cash out early?

- Verify the People: Are both primary and contingent beneficiaries listed and current?

With the fine print decoded, you are ready to determine exactly how these tools fit into your broader financial roadmap.

Mapping Your Strategy: How to Balance Legacy Protection with Lifetime Income

Financial planning need not be a tangle of jargon. You can now distinguish between the umbrella that protects your family from a storm and the steady paycheck that sustains a long retirement. This knowledge secures your life from two different directions, protecting against the risk of leaving too soon or living longer than expected.

Your next step depends on your current life stage. If you are in your peak earning years, prioritize building a protective wall for your dependents. Conversely, if you are approaching your golden years, calculate the “gap” between your guaranteed income sources, like Social Security, and your monthly bills. Deciding which is better for retirement income isn’t about picking a market winner, but about solving the specific math of your longevity.

Check your existing employer benefits first, as workplace coverage often provides a solid foundation before you buy private policies. While you may eventually explore estate planning with annuities, immediate success comes from identifying these coverage gaps. By matching the right tool to the right risk and by understanding both life insurance and annuities, you trade uncertainty for genuine financial control.

Not sure whether life insurance, an annuity, or a combination fits your goals?

Schedule a free, no-obligation consultation, and we’ll help you align the right tool to the right purpose—protection, income, legacy—based on your timeline and priorities.