Understand Annuity Disadvantages Before Committing

April 10, 2026

Annuity Disadvantages to Understand Before You Commit

Annuities are often sold as the ultimate financial safety net- a steady paycheck that lasts as long as you do. However, in the world of finance, you rarely get something for nothing, and the price of that “guaranteed” safety is often your flexibility and access to your own cash. While the promise of security is appealing, there are significant Annuity Disadvantages to Understand Before You Commit to such a binding agreement. These annuity disadvantages and annuity risks deserve careful review.

If you have been pitched an annuity, you have likely heard plenty about the benefits. Yet, before you sign a contract that could last decades, you need to understand what it takes away, including common annuity cons that limit control and liquidity. Unlike a standard bank account that acts like an ATM, an annuity functions more like a vault with a time lock. Industry standards typically dictate that once your money is deposited, accessing it for emergencies becomes difficult and expensive. Weighing the guaranteed lifetime income pros and cons requires looking past the sales brochure to the rigid reality of the contract, especially if the arrangement is a life annuity designed to pay as long as you live.

Many savers ultimately ask, “Are annuities a good investment for retirement?” The answer depends entirely on your willingness to accept specific trade-offs regarding how you control your money. Peeling back the layers of these complex products reveals the costs salespeople rarely highlight, helping you decide if the security is worth the price of admission—and whether the annuity disadvantages outweigh the potential benefits for your situation.

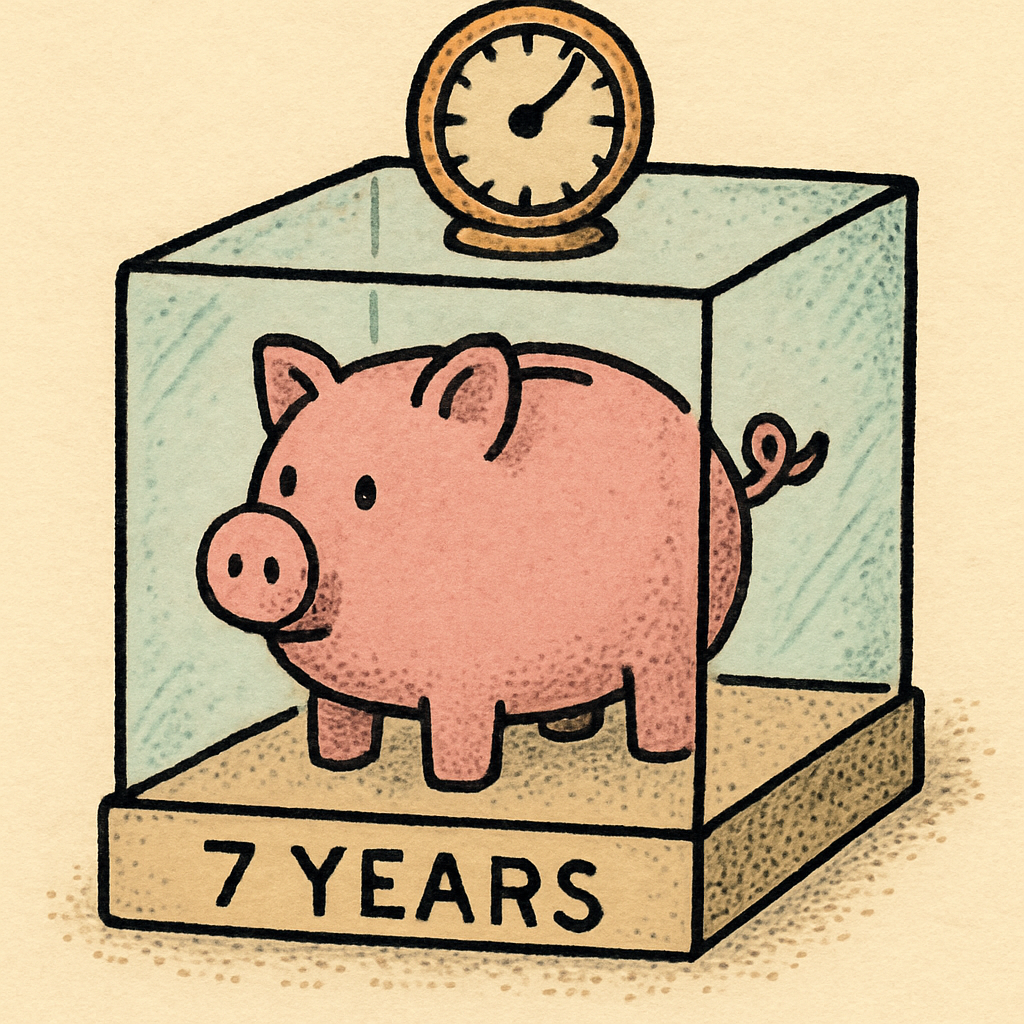

The 7-Year Lock-Up: How Surrender Charges Turn Your Savings Into a Locked Vault

Unlike a savings account, where your money is just a swipe away, an annuity functions more like a timed vault. When you hand over your lump sum, the insurance company effectively locks it away for a specific duration—often ranging from five to ten years. If life throws a curveball, such as a sudden medical expense or a necessary home repair, trying to access your full cash balance early triggers a steep penalty known as a “surrender charge.”

You might wonder why these penalties are so severe compared to other financial products. The reality is that the insurance agent who sold you the annuity likely received a large commission upfront—sometimes as high as 5% to 8% of your deposit. The insurance company pays this immediately, so if you try to exit the contract early, the surrender charge is their mechanism for recouping that commission directly from your principal.

Typically, this penalty acts on a sliding scale that slowly decreases over time until the contract matures. For a standard seven-year contract, the surrender charge schedule and penalties often follow this declining path:

- Year 1: 7% penalty

- Year 2: 6% penalty

- Year 3: 5% penalty

- Year 4: 4% penalty

- Year 5: 3% penalty

- Year 6: 2% penalty

- Year 7: 1% penalty

Most contracts do offer a small escape hatch called a “free withdrawal provision,” which usually allows you to take out 10% of your account value annually without a fee. However, relying on this limited liquidity can be dangerous if your financial needs suddenly exceed that cap. While these fees reduce your specific account balance today, there is another silent force that reduces what that money can actually buy in the future.

Why $2,000 Today Isn’t $2,000 Tomorrow: The Hidden Erosion of Fixed Payments

While surrender charges are an immediate penalty you pay for leaving, inflation is a slow-motion penalty you pay for staying. Most basic annuities offer a fixed monthly payment that never changes, creating what financial experts call “purchasing power risk.” A $2,000 check might cover your mortgage and groceries comfortably today, but in twenty years, the price of basics like energy and healthcare will likely have risen dramatically. You aren’t losing the actual dollars, but you are losing the ability to buy the same lifestyle you enjoy now.

To visualize this financial erosion, consider the impact of a standard 3% annual inflation rate. If you retire at 65 with a fixed benefit, by the time you reach age 90, that same check will only purchase about half of what it buys today. Your income effectively splits in two, just as your medical expenses often peak. This mathematical reality turns the promise of “guaranteed income” into a guarantee of a shrinking standard of living.

You can mitigate this danger by adding a Cost of Living Adjustment (COLA) rider, which automatically increases your payments annually. However, this protection forces a difficult trade-off: to get rising payments later, you must usually accept a significantly lower starting paycheck—often 20% to 30% less upfront. As you weigh the choice between a shrinking future income or a smaller current one, it is vital to also understand the confusing array of administrative costs that fund these products.

Decoding the ‘Layer Cake’ of Fees: Why Annuities Often Cost More Than Your 401(k)

If you look at your 401(k) statement, you likely see a single line item for “expense ratios,” often costing significantly less than 1% annually. Annuities, however, function less like a simple investment account and more like a layer cake of costs, where multiple fees stack on top of one another. Because these products blend insurance guarantees with investment sub-accounts, you aren’t just paying for money management; you are also funding the insurance company’s operations and risks.

The most confusing charge for new buyers is often the Mortality and Expense (M&E) fee. Unlike a mutual fund fee that pays for stock picking, this charge—typically around 1.25%—pays for the insurance guarantees, such as the promise that your beneficiaries will get a death benefit even if the market crashes. While this offers peace of mind, it acts as a constant drag on your balance regardless of how well your investments perform.

When you analyze the fine print, a variable annuity often carries annual fees exceeding 3%, usually broken down into these three distinct layers:

- Base Insurance Charge (M&E): The administrative fee covering the insurance “wrapper” and overhead.

- Investment Management Fees: The separate cost to manage the underlying mutual fund-like sub-accounts (similar to your 401(k) costs).

- Optional Rider Fees: Extra annual charges for add-ons like guaranteed income for life or long-term care protection.

High commissions create another hidden dynamic: products with the highest fees are often pushed the hardest by agents seeking those substantial upfront payouts. This heavy fee structure creates a significant “drag,” meaning your money must earn over 3% every year just to break even. Unfortunately, overcoming this hurdle is difficult when the contract also imposes strict limits on how much profit you are actually allowed to keep.

The Growth Ceiling: How Participation Rates and Caps Limit Your Upside

While high fees eat away at your balance from the bottom, distinct contract rules often place a lid on your potential profits from the top. This is most common in “indexed” annuities, which promise to track the stock market without risking your principal. The trade-off for this safety is a mechanism known as a “cap rate,” which sets a strict maximum on how much interest you can earn in a given year. If the stock market soars by 20% but your contract has a 5% cap, the insurance company keeps the remaining 15% spread to cover their own costs and profit margins.

Beyond simple caps, insurers use “participation rates” to further limit what lands in your account. A participation rate of 80% means that if the market index rises by 10%, you are only credited with 8%. Furthermore, these calculations almost always exclude dividends—the quarterly cash payouts companies make to shareholders—which historically account for a massive portion of the stock market’s total return. Because the insurance company holds the actual investments while you only hold a contract, those missed dividends stay with the insurer, creating a significant “opportunity cost” over a twenty-year retirement.

Ultimately, these limitations create a growth ceiling that can make it difficult for your savings to keep up with inflation. You might feel safe avoiding market crashes, but if your money stagnates due to caps and missed dividends, you lose purchasing power over time. Unfortunately, the restrictive nature of these contracts doesn’t end with growth limits; it extends to how the IRS treats the money when you pass it on to your children.

Tax Traps for the Unwary: Why Your Heirs Might Prefer Life Insurance

Most investors assume long-term savings receive special tax treatment, but annuities are subject to stricter rules. While profits from stocks held over a year enjoy lower “capital gains” rates, annuity earnings are taxed as “ordinary income”—the same higher rate applied to your wages. Furthermore, the IRS enforces a “Last-In, First-Out” (LIFO) rule here. This forces you to withdraw your taxable profit first before touching your tax-free principal, ensuring you pay taxes immediately upon accessing your cash.

This heavy tax burden follows the money even after you pass away, creating a distinct disadvantage for your heirs. If you leave a standard stock portfolio to your children, they typically get a “step-up in basis,” effectively erasing taxes on prior growth. Annuities offer no such reset. Your beneficiaries inherit the full tax liability, and because the payout is taxed as ordinary income, it could inadvertently push them into a higher tax bracket at the worst possible time.

Do not confuse an annuity’s “death benefit” with the tax-free payout of a life insurance policy. While life insurance proceeds are generally tax-free, an annuity death benefit is often just your remaining account balance, still carrying that deferred tax bill. Because these structural issues can significantly reduce what you leave behind, you must verify that the product actually fits your specific situation. Before you commit your life savings, you need to demand clear answers to five critical questions.

The Exit Strategy: 5 Questions to Ask Before You Sign the Dotted Line

An annuity isn’t inherently good or bad; it is a specialized tool that trades your flexibility for a predictable income stream. Possessing the insight to look past the marketing promises allows for an evaluation of the real price of those guarantees. Instead of viewing these contracts as a simple safety net, you can now assess if the loss of liquidity and potential growth is worth the security offered.

Before committing your savings, perform your own annuity suitability check. Use these specific questions to cut through the sales pitch and demand transparency from your advisor:

- What is the total annual fee percentage, including all administrative and rider fees?

- How much commission are you earning immediately on this sale?

- How many years is my money locked up in a surrender period?

- What is the specific cost for inflation protection riders?

- What is the current credit rating of the insurer?

Never forget that a “guarantee” is only as strong as the company backing it. Always research the credit risk of insurance companies using independent ratings from agencies like AM Best. If the product’s mechanics remain unclear after asking these questions, keep your wallet closed. The smartest retirement planning tips ultimately rely on a simple rule: never buy a financial product you do not fully understand.

Want to avoid costly surprises before choosing an annuity?

Schedule a free, no-obligation consultation, and we’ll walk through the fine print—fees, surrender charges, liquidity limits, and income tradeoffs—so you can make an informed decision.