Self-Funded Health Plans vs Traditional Insurance: Key Differences

May 25, 2026

What Is a Self-Funded Health Plan? Plan Comparison Guide

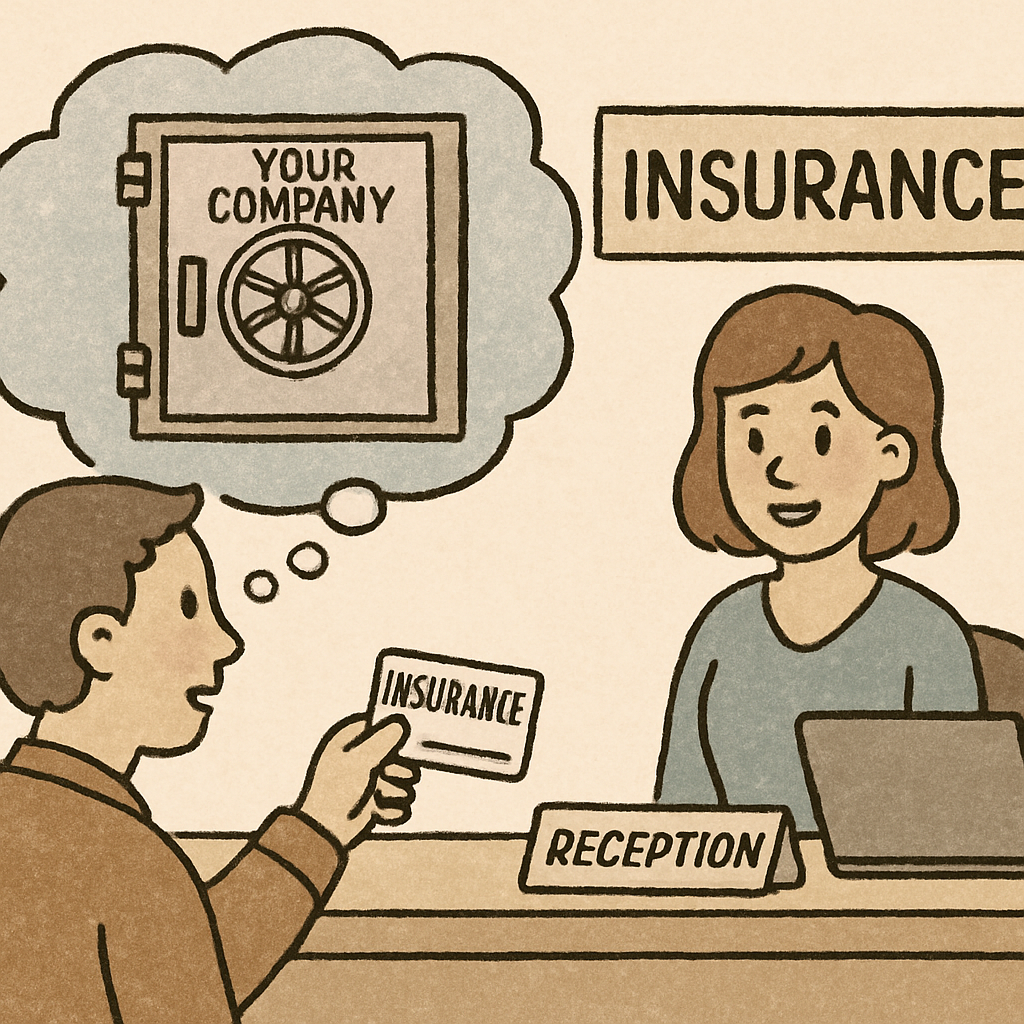

Handing your familiar ID card to a receptionist feels incredibly routine. You see a recognizable name like Aetna or BlueCross stamped on the plastic and naturally assume they cover your medical bills. Behind the curtain, however, a surprising reality exists for millions of workers. That massive insurance brand isn’t actually footing the bill for your visit; your employer is. In other words: What is a Self-Funded Health Plan? Don’t Confuse It With Traditional Coverage, because the employer, not the carrier, is funding actual care.

According to general industry trends, over 65% of large companies currently use this exact setup among their health insurance options. Instead of paying an insurer to assume all financial responsibility, businesses hire those famous brands simply to process paperwork and negotiate rates. For anyone trying to figure out who pays for claims in a self-funded plan, the funds come directly from your company’s own bank account.

Imagine putting your usual car insurance payments into a dedicated rainy-day fund. Should you get a minor dent, you pay for the repair out of those savings, but if you drive all year safely, you keep the cash. In a self-funded health plan, often called a self-funded health plan, the employer essentially becomes that bank, holding the money until someone actually needs a doctor.

Assuming this risk-bearing role might sound slightly dangerous for a business. Yet, operating a self-funded health plan allows companies to skip expensive traditional markups. Managing the risk themselves usually helps employers save money, which translates into more stable paycheck deductions and better, flexible perks for you.

The ‘Wallet Test’: How to Spot the Difference Between Paying a Premium and Funding a Claim

When you buy traditional private health insurance, you pay a fixed monthly bill regardless of whether you visit the doctor or stay perfectly healthy. This setup means your employer pays a massive premium that includes extra padding, often called “loading,” to cover the insurer’s overhead and profit margins. If no one at your company gets sick, the insurance company simply keeps that extra cash. This plan comparison ultimately shows who holds the risk and the wallet.

To stop losing those unspent funds, businesses weigh the fully insured vs self-funded health insurance pros and cons. The difference comes down to who holds the wallet:

- Fully Insured: The employer pays a fixed, padded monthly premium. The insurance company keeps any leftover profit.

- Self-Funded: The employer holds onto its own money, paying only for actual medical claims as they happen. The company keeps the savings.

Embracing the cash flow advantages of self-insured medical coverage allows a business to operate on a flexible, pay-as-you-go basis. Instead of financing an insurance company’s profit margin, your employer can use those retained funds to offer better workplace perks or keep your paycheck deductions lower. But if your employer is acting as the bank, you might wonder who actually processes the paperwork when you get sick.

Meet the Referee: Why You Still See Aetna or Cigna on Your Self-Funded ID Card

Looking at your insurance card, you might wonder why a familiar logo like BlueCross is still there if your employer is paying the bills. Often, employers rent a major insurer’s system through an Administrative Services Only (ASO) contract. In the ASO vs. self-funded insurance model, ASO is just the administrative engine inside the self-funded car. The big name doesn’t pay your medical bills; they simply provide the doctor network so your care remains uninterrupted.

Alternatively, your company might hire an independent middleman to act as a hired referee. The third-party administrator (TPA) role in healthcare involves enforcing the plan’s rules without actually providing the prize money. A TPA handles four essential tasks:

- Processing your medical claims

- Managing approved doctor networks

- Issuing your physical ID cards

- Answering customer service calls

Whether using an ASO or an independent TPA, this paper-pusher makes sure everything runs smoothly while your employer’s bank account funds the actual care.

The Catastrophe Umbrella: How Stop-Loss Insurance Protects Your Company (and Your Care)

Knowing your employer pays your medical bills directly might spark a frightening thought: what if three coworkers need million-dollar transplants this month? To prevent unexpectedly massive bills from bankrupting the company, employers buy a specialized safety net called stop-loss insurance. While the employer’s bank account pays for routine care, this backup policy covers true catastrophes, effectively managing financial risk in self-insured health plans.

Rather than relying on one generic safety net, companies divide their umbrella into two distinct layers of protection:

- Specific Stop-Loss (Individual Bills): This caps the financial hit from a single person’s medical emergency. If an employee’s premature baby requires $500,000 in NICU care, the employer might only pay the first $50,000, while the stop-loss policy covers the remaining balance.

- Aggregate Stop-Loss (Total Group Bills): This caps the company’s total healthcare spending. If a severe flu season causes everyone’s routine doctor visits to spike, this secondary policy kicks in once the entire group hits a pre-set yearly budget limit.

Because these safeguards catch both isolated disasters and overall budget overruns, they guarantee your medical claims get paid no matter what. With this financial armor safely in place, extra cash is suddenly freed up for exactly what comes next: lower premiums and better workplace perks.

Lower Premiums and Better Perks: The 3 Main Reasons Employers Ditch Traditional Insurance

With safety nets firmly in place, you might wonder why a company acts as its own bank. The answer comes down to escaping the hidden markups of traditional coverage. When paying a major carrier, a huge chunk of money goes toward the insurer’s profit margins and marketing budgets. Capitalizing on the cost savings of self-funded medical plans strips away these unnecessary expenses.

Self-funded health plans offer employers three distinct financial advantages:

- No state premium taxes: Traditional policies pay state taxes on every premium dollar. Self-funded plans are exempt, instantly saving companies a few percentage points.

- Custom health benefit design for employees: Instead of buying a rigid package, companies can tailor perks, like offering cheaper diabetes medications or expanded physical therapy.

- Keeping the float: If workers stay healthy and claims are low, the employer keeps the leftover cash instead of surrendering it as carrier profit.

This direct payment structure unlocks full data transparency. Seeing anonymous claims patterns helps companies identify wasteful spending, like frequent emergency room visits for simple colds, and proactively offer free telehealth alternatives. Because the employer writes the checks, they ultimately dictate the coverage. However, operating outside the standard insurance marketplace means following a different legal playbook.

Understanding the ERISA Shield: Why Your Plan Rules Might Differ from State Insurance Laws

Suppose you live in New York, but your coworker is in Texas. Normally, traditional insurance follows local state laws, meaning coverage requirements vary widely across borders. But when a company self-funds, they operate under a federal law called the Employee Retirement Income Security Act (ERISA). This acts as a legal shield, allowing the employer to bypass a patchwork of state mandates and offer one consistent plan to everyone.

Managing separate rulebooks is a logistical nightmare for expanding companies. Maintaining ERISA compliance for self-insured employers solves this by creating a single, nationwide standard. If a business has offices in multiple states, they don’t juggle different medical regulations. Instead, the federal government oversees your benefits, ensuring claims are handled fairly and your healthcare funds are protected, regardless of your zip code.

Because of this federal umbrella, your benefits might not include a highly specific local mandate, but it guarantees an equitable package for all workers. It is a powerful setup for large corporations, though acting as a bank can still feel risky for smaller shops. Fortunately, these smaller companies have a safer stepping stone called level-funding.

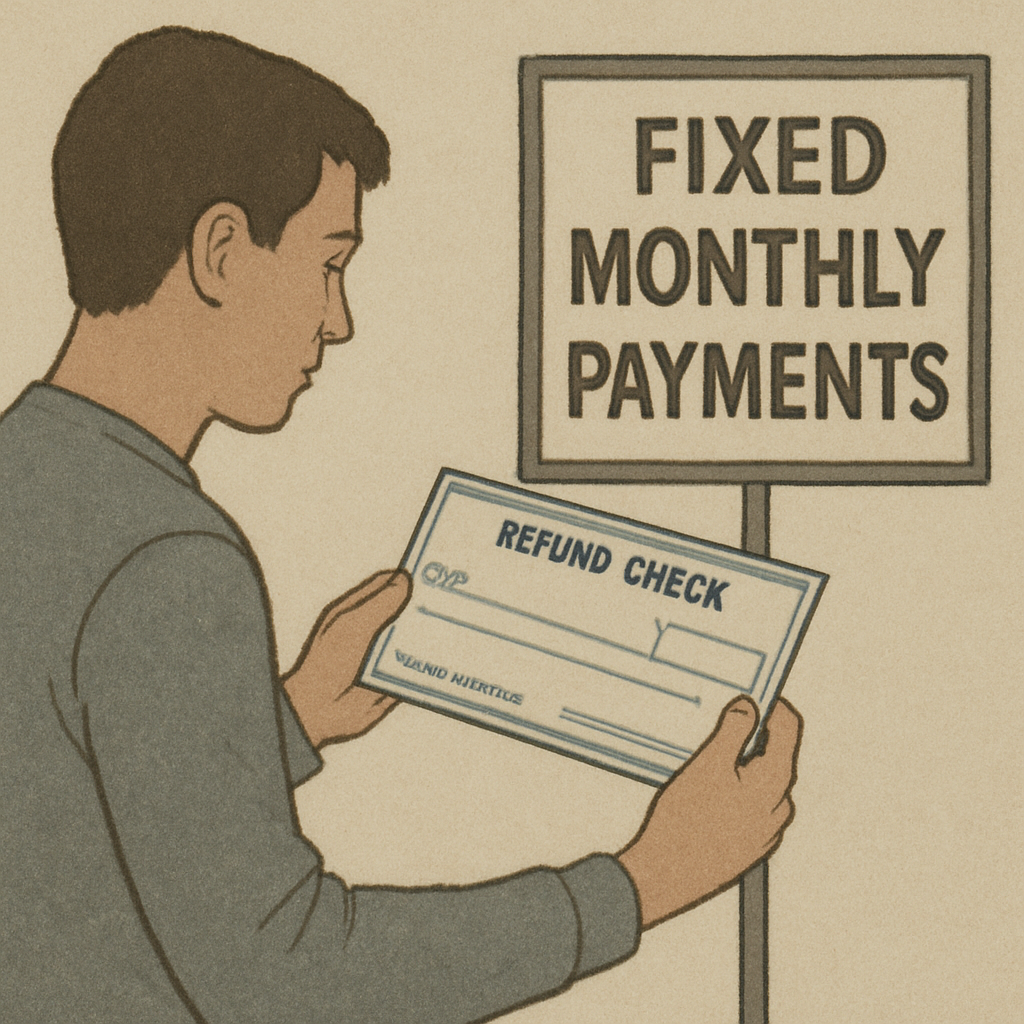

Level-Funding for Small Businesses: The Halfway House Between Traditional and Self-Funded

Imagine managing your company’s healthcare like a strict household budget. Small businesses often want the flexibility of a self-funded health plan, but they desperately need the predictable monthly bills of standard coverage. When evaluating level-funded vs fully insured health plans, the level-funded model acts as the perfect halfway house. The company pays a fixed monthly amount, protecting them from sudden cash crunches if multiple employees get sick simultaneously.

Instead of losing that predictable payment to a massive insurance carrier, the money goes into an employer-controlled account. Here is the typical year-end scenario for a level-funded setup:

- Pay monthly: The employer contributes a steady, fixed amount each month.

- TPA pays claims: A third-party administrator uses this account to cover doctor visits and pharmacy bills.

- Get a refund: If the team stays healthy, the business gets the unused surplus back.

Receiving a refund check instead of boosting an insurer’s profit margin is exactly why this model is skyrocketing for smaller shops. However, if medical claims completely drain that account, a unique financial safety net is required to handle massive bills.

Managing the Risk: Who Actually Pays for a $100,000 Hospital Bill in a Self-Funded Plan?

When a surgery generates a massive $100,000 hospital bill, your first defense is a familiar one: network discounts. Although your employer funds the plan, they essentially “rent” access to major provider networks. Because the hospital is in-network, that terrifying six-figure bill gets immediately slashed to a negotiated rate before anyone pays a dime.

Next comes the paperwork phase, which reveals how a self-funded health plan works behind the scenes. The hospital sends this discounted bill to the Third-Party Administrator (TPA). The TPA acts as an independent referee, performing a process called claim adjudication. This simply means they verify the medical bill against your specific plan’s rules to accurately calculate what you owe.

After the math is settled, the payment sequence begins. For routine care, the TPA pulls cash straight from the employer’s dedicated healthcare account. However, managing financial risk in self-insured health plans requires a safety net for catastrophic moments. If the employer’s portion exceeds a specific dollar threshold, their protective stop-loss insurance kicks in to cover the rest.

Throughout this financial relay race, your patient experience remains completely seamless. You pay your normal deductible, the hospital gets fully funded, and the business stays safe. With this invisible safety net in place, companies can safely transition from premium payers to plan owners.

From Premium Payer to Plan Owner: The 4 Steps Companies Take to Self-Fund Responsibly

Leaping from paying premiums to a massive insurance company to running an internal healthcare “bank” doesn’t happen overnight. For a business, the steps to transition from fully insured to self-funded require careful planning, usually taking six to twelve months of data-driven decision-making.

To build this custom plan safely, companies follow a precise four-stage playbook:

- Feasibility Study: Employers analyze their “experience rating,” a summary of past medical claims data, to mathematically prove if taking on their own risk makes financial sense.

- Selecting TPA/Network: They hire a Third-Party Administrator to handle the daily paperwork and provide access to a major doctor network.

- Buying Stop-Loss: They purchase a catastrophic insurance policy to shield the business checking account from unpredictable, million-dollar hospital bills.

- Employee Communication: HR explains the transition, ensuring you know exactly how to use your new ID cards.

After completing this timeline, the custom structure goes live invisibly, usually leaving you with identical or better coverage.

Take Control of Your Benefits: 3 Vital Questions to Ask Your HR Department Today

You no longer have to view your benefits card as a mystery. Recognizing that your employer might be acting as the bank, rather than simply buying standard private health insurance, empowers you to make informed decisions during any plan comparison or review of health insurance options.

In a self-funded model, your transparent choices matter. When you use a generic drug or an urgent care clinic, you directly protect your company’s funds, which ultimately helps keep your future premiums low and preserves your workplace perks.

Turn this insight into action by taking these three questions to your HR department:

- Are we self-funded or level-funded?

- What TPA network do we use?

- How can I help keep healthcare costs down?

Asking these questions makes you an active participant in your healthcare. Instead of fighting an invisible system, you are now equipped to use your coverage wisely, protecting both your health and your wallet.

Q&A

Question: What is a self-funded health plan, and how is it different from a fully insured plan?

Short answer: In a self-funded plan, your employer pays medical claims directly from its own bank account as they occur, instead of paying a fixed monthly premium to an insurer. The company keeps any savings if claims are low, gains data transparency, avoids state premium taxes, and can customize benefits. By contrast, in a fully insured plan, the insurer takes the risk, charges a padded premium (including overhead and profit), and keeps any leftover funds. You may still see a big-brand logo on your ID card because that insurer (or a third-party administrator) is just handling administration and network access, not paying your claims. Over 65% of large companies use some form of self-funding.

Question: What protects a self-funded employer (and my care) from huge, unexpected medical bills?

Short answer: Stop-loss insurance is the safety net. It has two layers: Specific stop-loss caps the cost tied to any one person’s claims (e.g., the employer pays the first set amount, and the stop-loss carrier pays the rest), while Aggregate stop-loss caps the plan’s total annual spend if group-wide claims surge. Together, they prevent catastrophic costs from overwhelming the employer and help ensure your claims are paid.

Question: How does a big medical bill, say $100,000, actually get paid under a self-funded plan?

Short answer:

- The bill is first reduced to a negotiated in-network rate.

- The hospital sends the discounted claim to the plan’s third-party administrator (TPA), which adjudicates it against your plan rules.

- You pay your normal cost share (deductible/coinsurance).

- The TPA pays the provider from the employer’s healthcare account for the covered portion.

- If the employer’s responsibility exceeds the plan’s specific stop-loss threshold, stop-loss insurance covers the rest. Your experience remains seamless.

Question: Do self-funded plans have to follow my state’s insurance mandates?

Short answer: Generally, no. Self-funded plans operate under the federal ERISA law, which preempts most state insurance mandates. That lets employers offer one consistent plan nationwide and have federal oversight of benefits and fiduciary protections. The trade-off is that some highly specific state mandates may not apply, but employees across states receive a uniform benefit design.

Question: What is level-funding, and who is it best for?

Short answer: Level-funding is a “halfway house” between fully insured and self-funded plans, often used by smaller employers. The company pays a predictable, fixed monthly amount into an employer-controlled account; a TPA pays claims from that account; and if claims run low, the employer may receive a refund of unused funds. If claims are high, built-in protections and stop-loss-like coverage stabilize cash flow. It delivers some self-funding advantages (potential refunds, more flexibility) while preserving the budgeting certainty of fixed monthly payments.

Q&A

Question: Why does my ID card show Aetna, Cigna, or BlueCross if my employer is paying the claims?

Short answer: Many self-funded employers “rent” a big insurer’s network and admin tools through an Administrative Services Only (ASO) contract or hire an independent Third-Party Administrator (TPA). These partners process claims, manage provider networks, issue ID cards, and handle customer service, but they don’t pay your medical bills. Your employer’s bank account funds the care; the brand on the card is the administrative engine and network access.

Question: How do self-funded plans protect against catastrophic, budget-breaking medical costs?

Short answer: Employers buy stop-loss insurance as a financial backstop. Specific stop-loss caps the employer’s exposure to any one person’s high-cost claims (the carrier pays above a set threshold), while aggregate stop-loss caps the plan’s total annual spend if overall claims spike. Together, they keep the company solvent and ensure claims get paid even in extreme scenarios.

Question: What advantages do self-funded plans offer, and how might employees feel the benefits?

Short answer: Self-funding avoids state premium taxes, lets employers customize benefits (e.g., lower-cost diabetes meds or expanded physical therapy), and allows them to keep savings when claims are low (“the float”). With full claims transparency, employers can curb waste (like unnecessary ER visits) and add cost-saving options (e.g., telehealth). The result often shows up as more stable paycheck deductions and better, more flexible perks.

Question: What does ERISA change about my coverage compared to state-regulated insurance?

Short answer: Self-funded plans are governed by the federal ERISA law, which generally preempts state insurance mandates. That lets multi-state employers offer one consistent plan nationwide with federal oversight and fiduciary protections. Some highly specific state mandates may not apply, but employees across locations receive a uniform benefits package.

Question: What is level-funding, and how does it work over the year?

Short answer: Level-funding is a hybrid model popular with smaller employers. The company pays a fixed monthly amount into an employer-controlled account; a TPA pays claims from it. If claims run low, the employer may receive a year-end refund of unused funds; if claims run high, built-in protections (similar to stop-loss) stabilize cash flow. It delivers self-funding’s potential savings and flexibility with the predictability of fixed payments.

Not sure how a self-funded plan compares to fully insured coverage, and what it means for your costs?

Schedule a free, no-obligation consultation, and we’ll help you break down plan structure, risk, and real-world costs so you can choose coverage with confidence.